The Hidden Psychology of Change: How We Value Gains and Losses

Understanding the Role of Loss Aversion and Risk-Seeking When Facing Losses

This is The Curious Mind, by Álvaro Muñiz: a newsletter where you will learn about technical topics in an easy way, from decision-making to personal finance.

Have you ever wondered why it is so hard to change jobs?

Changing jobs, moving homes, or making life decisions always come with trade-offs: gains and losses. A higher salary might mean fewer vacation days; a bigger house could be in a less desirable location. Why are these decisions so hard?

Because losses feel worse than gains feel good.

Today in a nutshell

Prospect Theory is a theory in behavioural economics and cognitive science developed by Daniel Kahneman and Amos Tvesrky in 1979.

Whereas utility theory assigns some value to a given wealth, prospect theory deals with changes in wealth: wins and losses.

One of its main observations is that humans are loss averse: we dislike losses more than we like winnings.

Utility Theory: The Classical Approach to Decision-Making

Some weeks ago we discussed the concept of the utility of money.

The utility of money is the value we assign to a given amount of money. One of the key insights was that the value we assign to something like $100 depends on our current wealth. This forced us to be risk-averse, preferring certain outcomes to uncertain ones.

Utility theory was, for a long time, the major theory in behavioural economics. It was assumed that a rational person should take decisions according to utility: given two alternatives, they would choose the one that delivers the most utility. It is a simple theory and works really well in most situations, but it has some problems.

What Utility Theory Can’t Explain

Gains vs Losses

Utility theory assigns value to some amount of money. This misses a crucial point, which is what was your previous state. Consider the following example:1

Jack and Will have now the same wealth, and thus the same utility. According to utility theory, they should value their money the same way. Yet any of us know that we would not feel the same in both situations. Will just lost money, decreasing his wealth, whereas Jack just won money, increasing his health.

Imagine this as your yearly bonus. If your bonus increases from $1,000 to $5,000, you’ll be thrilled. But if it drops from $9,000 to $5,000, you’d feel cheated—even though both outcomes leave you with the same amount!

Utility theory does not deal with gains or losses, just with the final state.

Risk-seeking

Consider the following examples:2

When discussing utility theory and risk aversion, we saw that most people would choose to win $900 for sure. We prefer sure wins to potential ones, even in cases where the potential win is larger.

Now consider instead the following scenario:

In this case, most people would choose the gamble. This is the opposite to risk aversion: we prefer potential losses to certain ones, even in cases where the potential loss is larger. The sure loss is very aversive, and it drives you to take the risk.

This risk seeking behaviour cannot be explained by utility theory, where one always prefers certain outcomes to uncertain ones.

When all options are bad, humans tend to be risk-seeking and prefer the gamble.

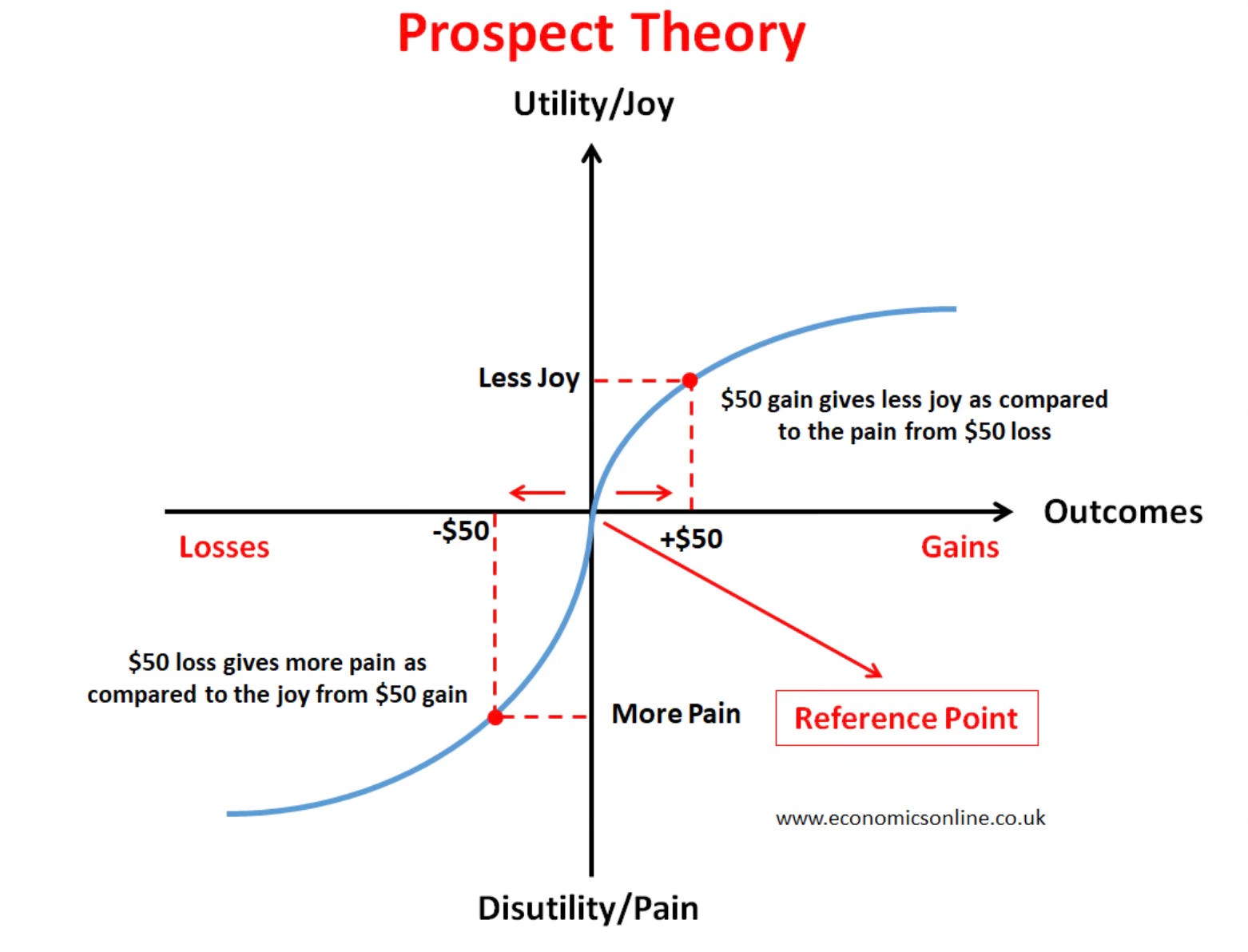

Prospect Theory

In 1979, Daniel Kahneman and Amos Tversky developed a theory that tried to explain the defaults of utility theory. They named it Prospect Theory, and it contributed to Kahneman winning the Nobel Prize in 2002.

Their key insight was that we should look at changes in wealth rather than just at the wealth itself, and that we do not value a gain the same way as we value an equal loss.

We can summarise their theory in the following three axioms:

Axioms of Prospect Theory

We should evaluate wealth with respect to a reference point.

Gains in wealth are perceived as less valuable the more we have: going from $100 to $200 is subjectively more valuable as going from $900 to $1,000.

On the other hand, the opposite happens with losses: going from $1,000 to $900 feels worse than going from $900 to $800.Given a gain and a loss of the same magnitude, the loss looms larger than the gain.

We illustrated the first point before: we saw that it is not just the end wealth that matters, but also whether it is above or below your previous wealth (the reference point).

The first part of the second point—that gains in wealth bring diminishing utility—is something that we discussed already when talking about utility theory. The second part—that losses in wealth cause a diminishing pain—is the reason why, if you are given the choice to lose $900 or to gamble to lose $1,000 or to lose nothing, you probably take the gamble.

To understand the third point, consider the following example:

The expected value of this game is positive: on average, you win $10 (you win $120 half of the time, and lose $100 half of the time, so, on average, you get 0.5 x $120 + 0.5 x (-$100) = $10). Yet, most people would probably not want to play this game.

The pain of losing $100 outweighs the joy of gaining $100—even the joy of gaining $120. This is loss aversion.

You can measure how loss averse you are by answering the following question:

How much would you need to be offered when the coin shows tails to accept the deal?

For most, people, this is around $200. That is, we perceive losses twice as strong as we perceive wins.

This gets higher and higher as the loss increases. If the coin showing heads made you lose $10,000, would you accept a deal that gives you $20,000 when it shows tails? Probably not—you will know ask for significantly more reward.

Conclusion

Understanding Prospect Theory helps explain why life changes—like switching jobs—feel so daunting. It’s not just about the numbers; it’s about how we perceive gains and losses.

By recognizing our loss aversion, we can make better, more rational decisions in the face of uncertainty.

What’s coming:

Rabin’s theorem and the absurdities of utility theory

Limitations of Prospect Theory

In case you missed it:

From Profit to Utility: Approaching Risk in Financial Decisions

Profit vs. Risk: What Betting Games Teach Us About Human Decision-Making

How You Can Make Better Choices (Spoiler: Self-Interest Fails)

What do you want next?

I got this example from Thinking, Fast & Slow by Daniel Kahneman.

Also from the same book.

I'm definetly way too risk averse haha I would need to be offered 1000$ in order to want to flip the coin 😅😂